Monday Fun Day

morning musings 4.27.26- views from the island

“The words of the prophets are written on the subway walls and tenement halls” ~Simon and Garfunkel

I’m reeeeal tired of this..I mean 40 and rainy on April 25? I gotta re-think this NJ thing

Kenya’s Sabastian Sawe shatters two-hour marathon mark to win in London.

Markets are navigating a critical week featuring major megacap tech earnings and central bank decisions, with uncertainty persisting that U.S. and Iran could come to deal to restore Middle East oil flows . Brent crude rose 2.5% to around $108 a barrel as the Strait of Hormuz remained largely shut after two months .

5 of the Mag Seven report this week, with little room for error after the group has risen nearly 20% since late March .

Global Central Bank Hold Pattern: All G-7 central banks meet this week and are expected to hold rates steady while monitoring Iran war fallout, with the Fed, BOE, ECB, BOJ, and Bank of Canada all likely to maintain current policy; Iran standoff is forcing central banks to navigate stagflationary risks, with the ECB, Fed, and Bank of England all expected to hold rates steady this week despite elevated inflation pressures

China’s decision to block Meta’s $2 billion acquisition of Manus sends a chill through the AI sector just weeks before the Trump-Xi summit.

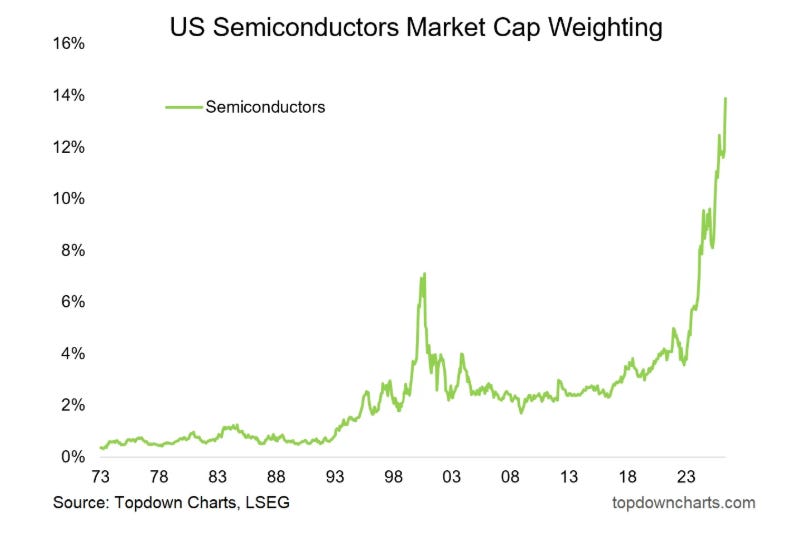

Semis climbed for a record 18th straight session, with Intel soaring 28% Friday on blowout results and Nvidia closing at a new record .

AI Infrastructure & Deployment: The next phase of the AI buildout depends heavily on Asia’s hardware ecosystem, including chips, memory, advanced packaging, semiconductor equipment, precision manufacturing, power and data centers . 61% of manufacturers are already in active AI deployment—not piloting, not planning, deploying . 70% of enterprise AI is uncontrolled, driving hidden risk, cost and slower ROI. The AI story is no longer just about U.S. mega caps, as the next phase of the AI buildout depends on the entire supply chain in Asia . Tech companies are rushing to trade their people for more chips, with Microsoft and Meta Platforms scaling back their workforces in the name of artificial intelligence . Meta’s latest plans will cut about 8,000 people from its workforce.

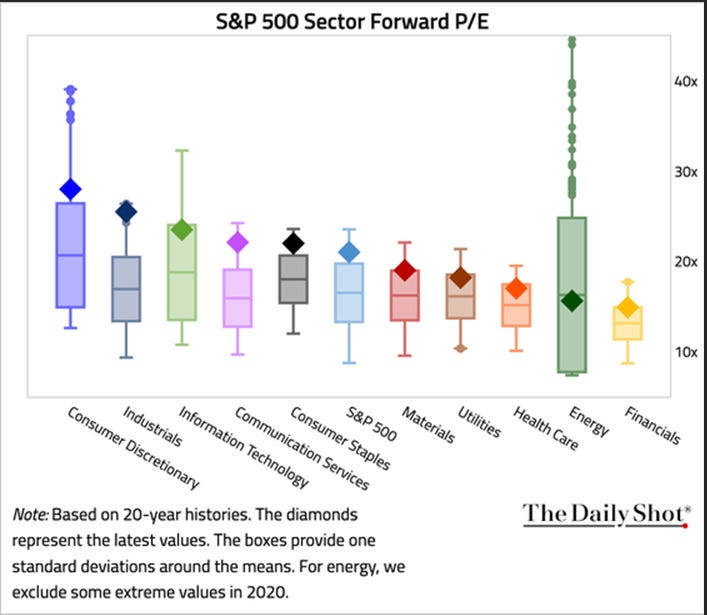

Oppenheimer Asset Management upgrades U.S. utilities and financials to outperform, with the upgrade to financials based on improved prospects for the sector .

Financials Sector

2s10s curve most normal since 2022 -- net interest margin tailwind for banks builds gradually as loans reprice. With Warsh advancing to confirmation, market should begin pricing a more hawkish-leaning Fed longer-term, which could pressure bank fixed-income books but benefit deposit franchises.

Secondary PE valuation disconnect (per First Look) -- NAV marks vs. secondary market clearing prices diverging; potential write-down risk for PE-exposed financial intermediaries.

Q1 earnings for financial names reporting this week (V on Tue 4/28, MA on Thu 4/30) -- card network volumes will be the read-through for consumer spending resilience.

IG credit spreads ~80bp, near multi-decade tights. HY at ~285bp. PineBridge noted potential for widening given thin cushions and surge in long-duration supply from tech/M&A.

RATES & CREDIT:

FOMC meets Wednesday-Thursday with no rate move expected; the market’s focus will be on forward guidance language and any acknowledgment of the Warsh transition.

PCE Price Index prints Thursday alongside the FOMC decision -- a hotter-than-expected PCE could complicate any dovish lean.

COT data (week ending April 21) shows hedge fund gross USD long reduced 20% to $11.7B from a 14-month high -- speculators are net sellers of the dollar for a second consecutive week, supporting EUR and MXN. JPY net short reached a 21-month high at $7.4B -- a crowded trade vulnerable to BOJ surprise at this week’s meeting.

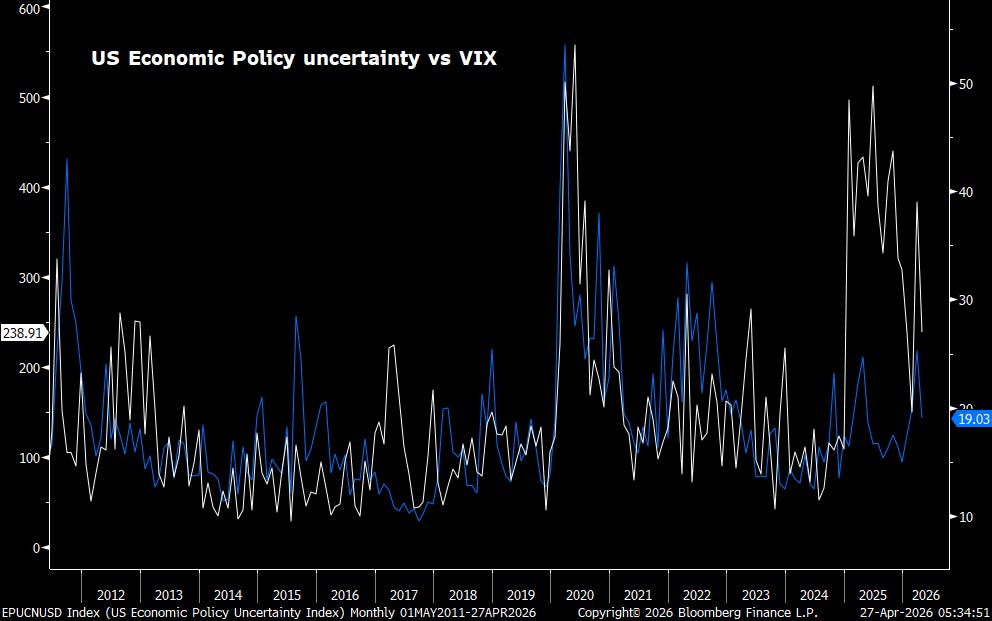

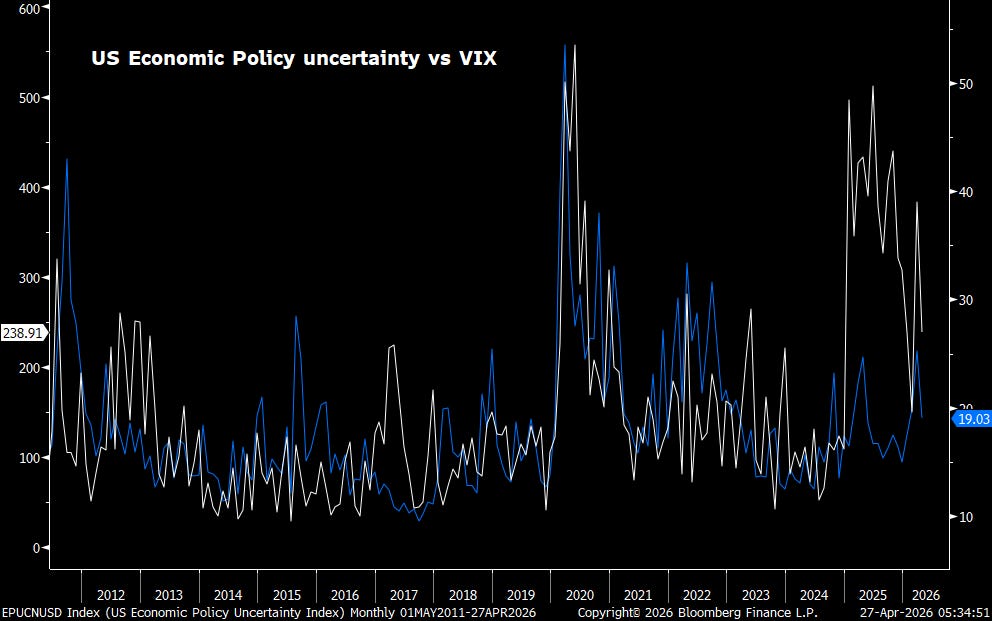

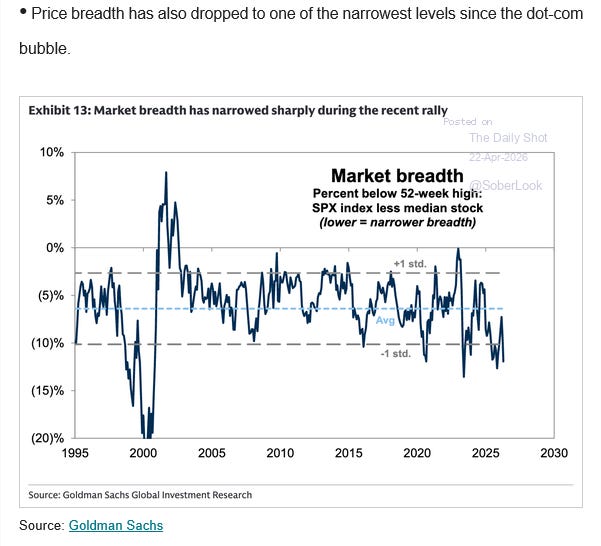

OK, so let’s start with the markets. There is definitely (IMHO) a belief that US policy is ‘guard-railed)‘ by market reaction; think bowling alley lane bumpers. More random on the upside ( who doesn’t want new highs! yadayadayada) but clear on the downside. Ego, VIX well below economic uncertainty

Meanwhile, given this clear ‘support’ on every selloff, and with a cataracted eye towards energy/petrochemical implications ( more on this below), markets continue to have a bullish hue. This dissociation has allowed focus to stay on traditional fundamentals and ‘looking at the long term’ with an implicit diminution of the Iran excursion; ceteris paribus, the market is attractive. Again, perhaps this is the case. Perhaps there is a global reordering, and the US IS reading the board well and making the appropriate strategic plays. But there is massive downside tail risk and significant short-term economic impact already baked in because of supply delays, which the market seems to be ignoring.

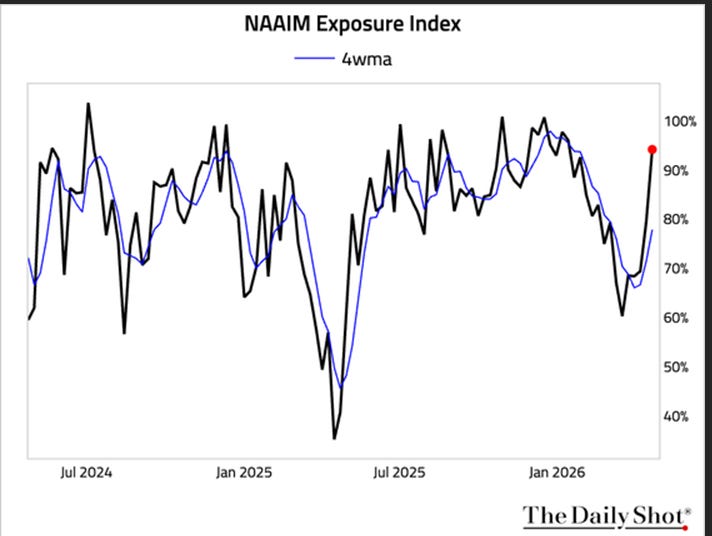

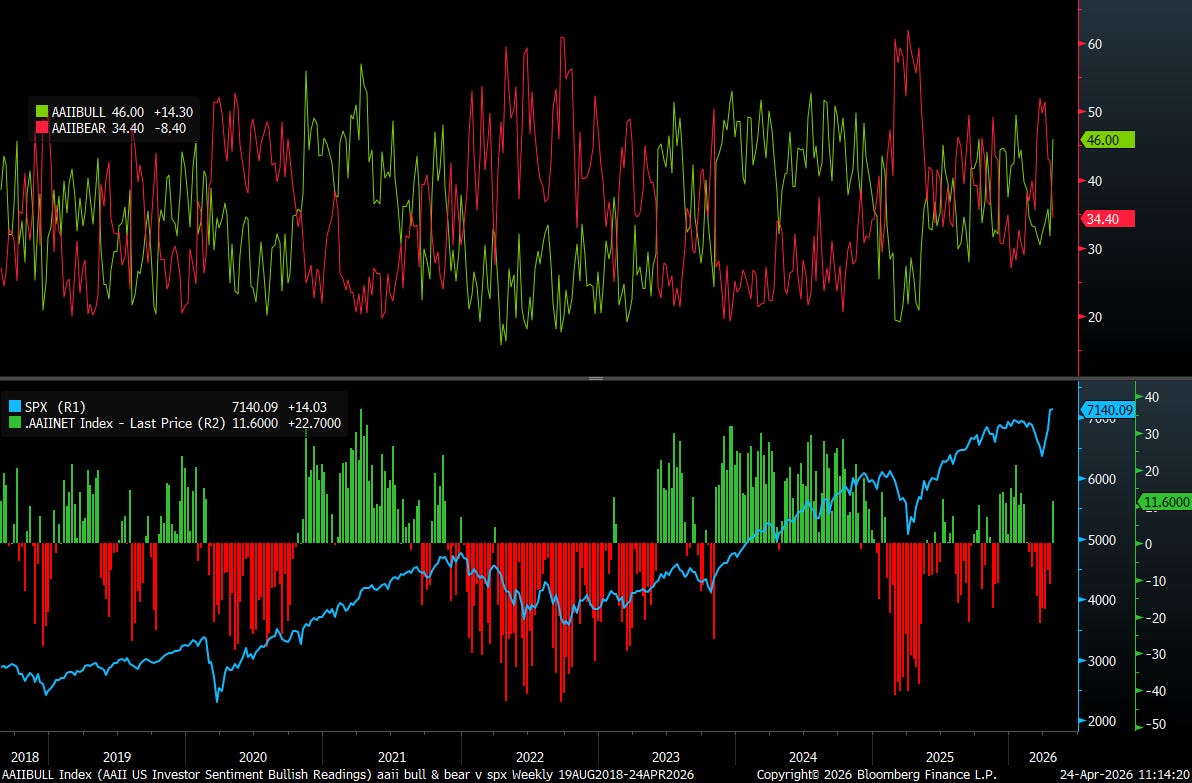

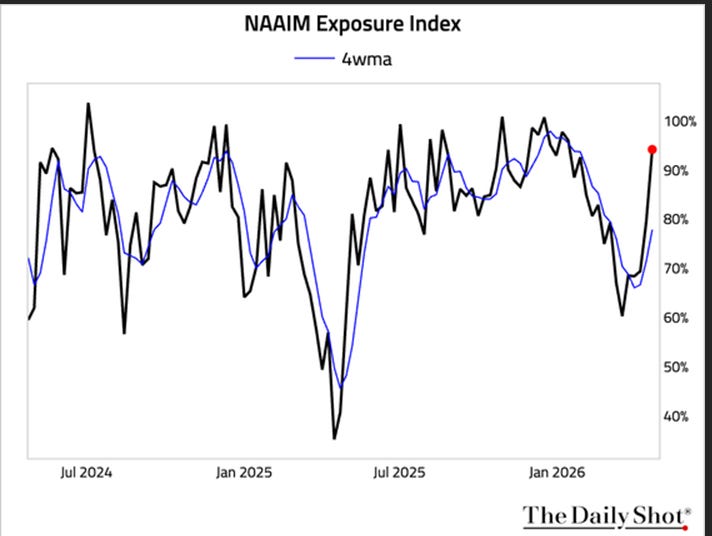

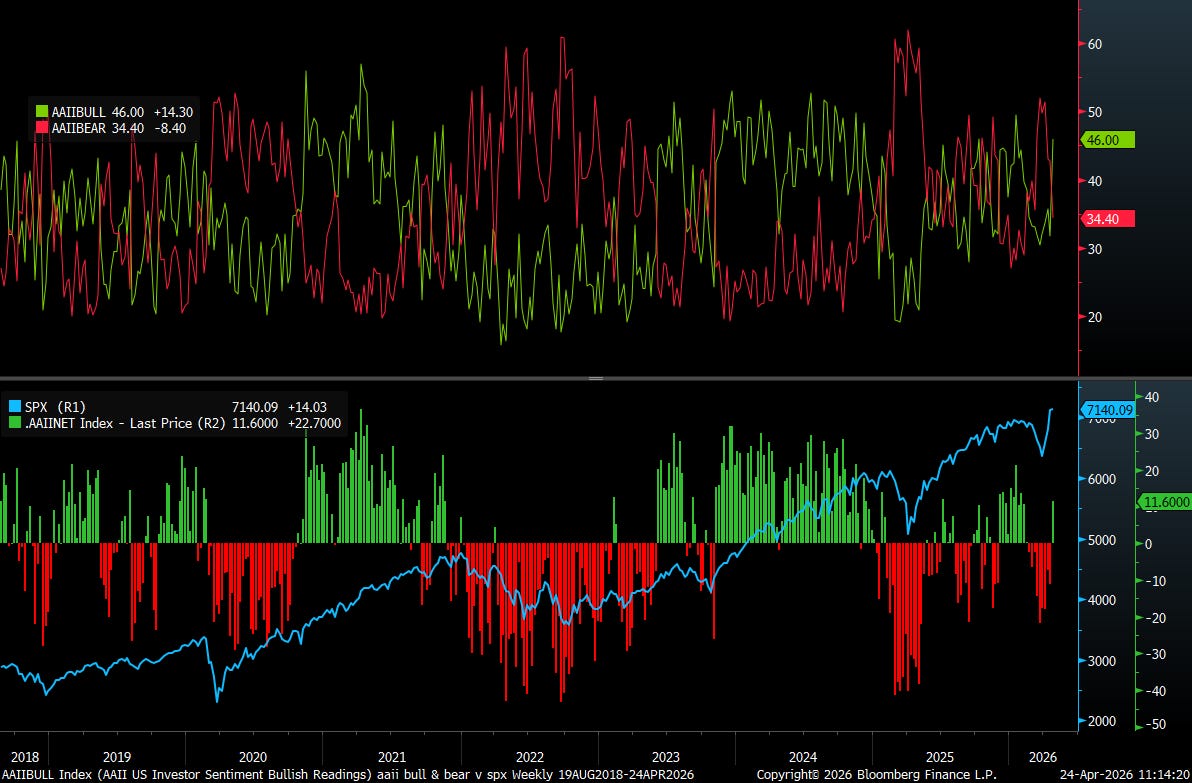

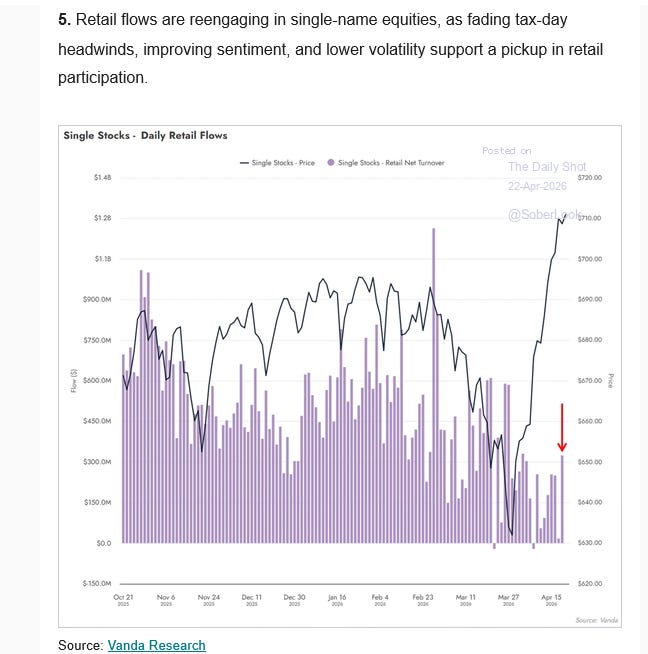

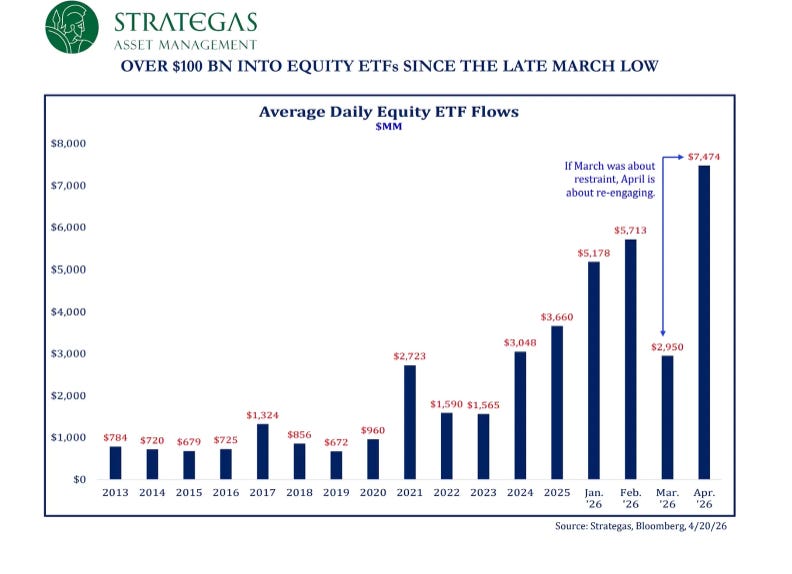

Add to this the growing importance of passive/CTA/systematic/mechanical investment processes, and the need for active managers to ‘beat their bogies’, and voila, active managers adding, retail is back, and even investor sentiment is creeping higher.

And in the background…

Middle East

‘ Iran’s Foreign Minister Abbas Araghchi arrived in Russia for today’s meeting with President Vladimir Putin in Saint Petersburg.

Araghchi said his trip to Russia would provide a key opportunity to review war developments and coordinate positions, according to the Mehr news agency. He said his earlier stop in Islamabad was necessary because Pakistan is involved in mediation, where he said talks made some progress but failed to achieve their aims due to “excessive demands” by Washington.

Some may say that perhaps Putin will provide Araghchi with useful tips how to deal with Trump, who seems to have a soft spot for the Russian president.

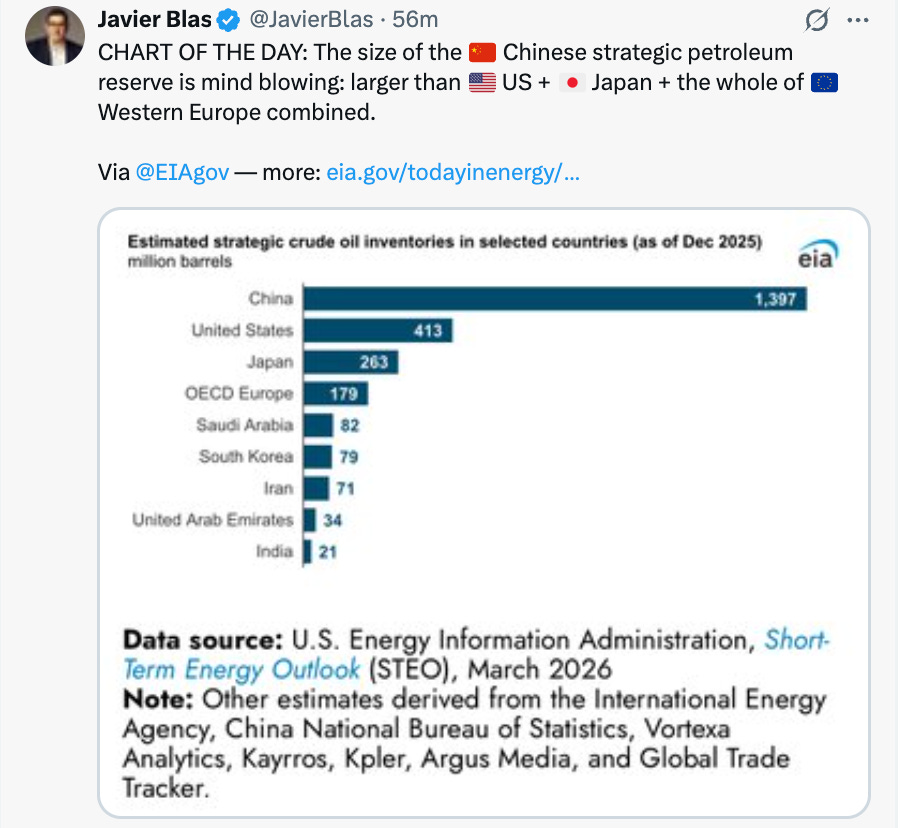

Since the Iran war began in late February, the United States has burned through around 1,100 of its long-range stealth cruise missiles built for a war with China, close to the total number remaining in the U.S. stockpile. The military has fired off more than 1,000 Tomahawk cruise missiles, roughly 10 times the number it currently buys each year.

The Pentagon used more than 1,200 Patriot interceptor missiles in the war, at more than $4 million a pop, and more than 1,000 Precision Strike and ATACMS ground-based missiles, leaving inventories worrisomely low, according to internal Defense Department estimates and congressional officials.

The Iran war has significantly drained much of the U.S. military’s global supply of munitions, and forced the Pentagon to rush bombs, missiles and other hardware to the Middle East from commands in Asia and Europe. The drawdowns have left these regional commands less ready to confront potential adversaries like Russia and China, and it has forced the United States to find ways to scale up production to address the depletions, Trump administration and congressional officials say. (Read the rest. Sources: nytimes.com, wsj.com)

Iran's new proposal to reopen the Strait of Hormuz and end the war; President Trump canceled planned envoy visits to Pakistan over the weekend. Iran offered to end its chokehold on the Strait of Hormuz without addressing its nuclear program; it also wants the United States to end its blockade of the country as part of its proposal

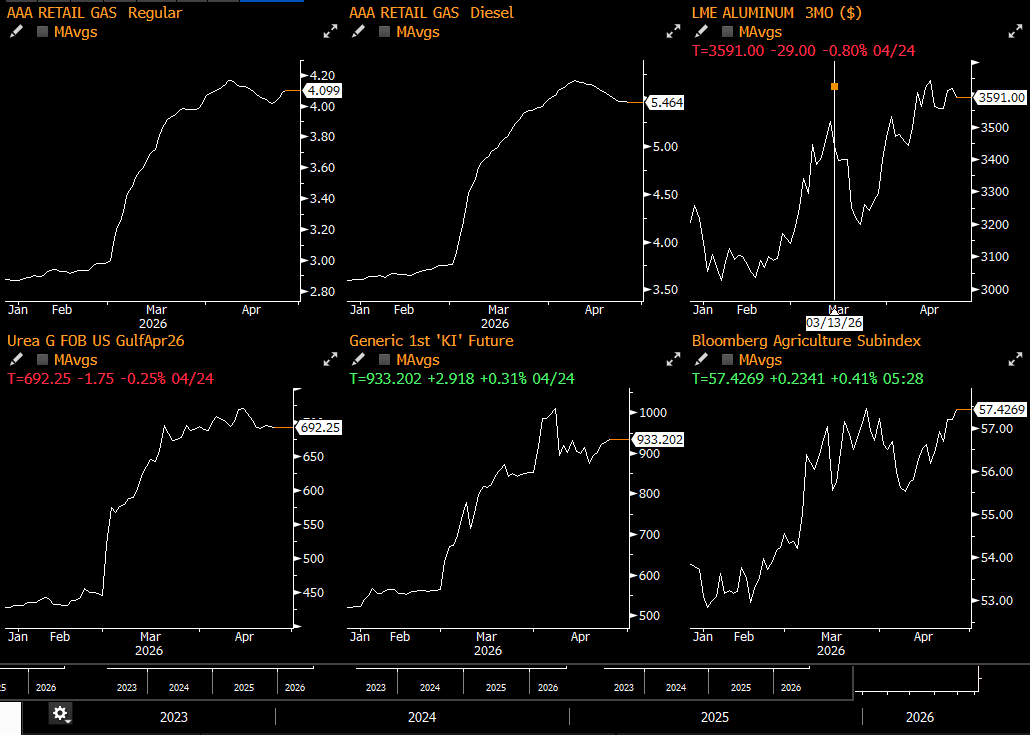

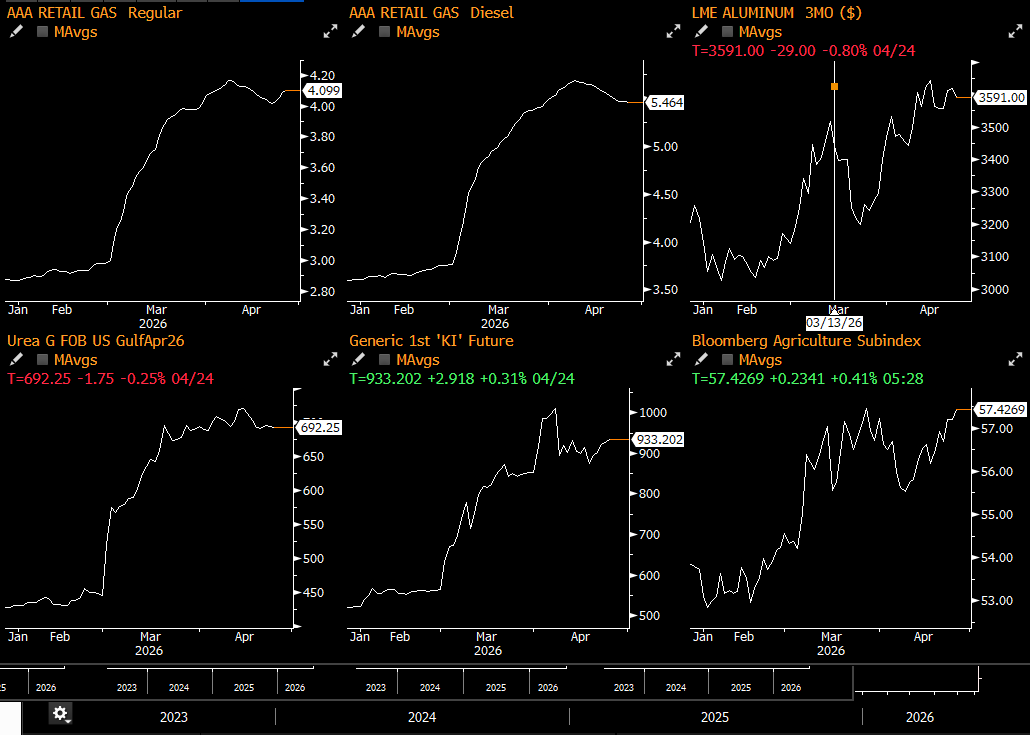

Brent +$2 following stalled negotiations. Goldman Sachs raised its year-end Brent forecast to $90/barrel from $80, citing lower Gulf output and longer-than-expected disruptions.

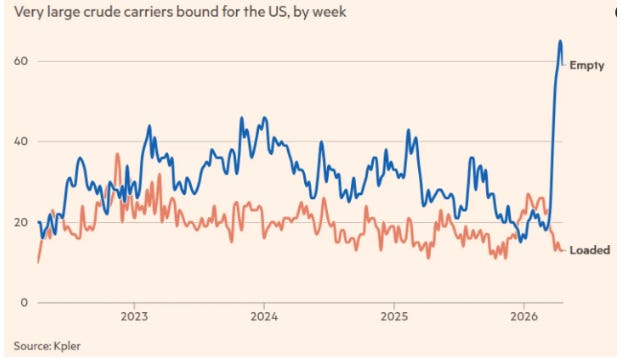

European natural gas prices fluctuating after surging over 90% since Friday’s close, while Asian refiners contemplate 20-30% run rate cuts as dozens of crude tankers remain stranded in the Persian Gulf.

Iran announced measures to curb natural-gas consumption, as it prepares to repair damage from Israeli airstrikes inflicted on its facilities associated with its South Pars gas field. According to experts, Kharg Island storage is now full, which will necessitate shut-ins (which have long term supply ramifications)

War heading into a ninth week has kept oil prices elevated supply chain issues continue to worsen.

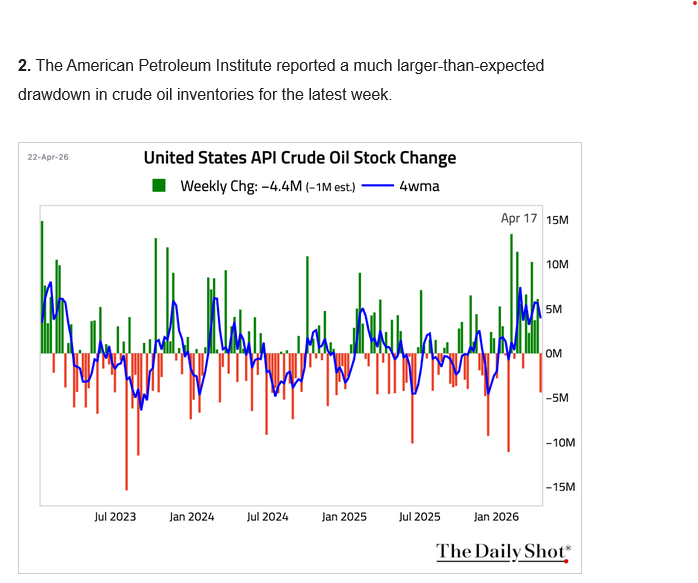

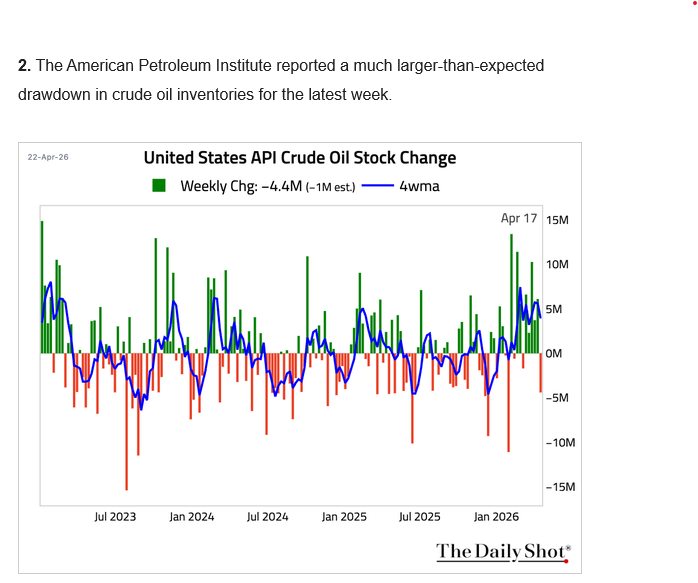

The conflict is already damaging the economy through elevated oil prices and snarled supply chains; the blockage has tightened global supplies across crude, refined fuels, petrochemicals, metals, and fertilizers. COT data (Ole Hansen/Saxo, week ending April 21) shows combined crude oil net long already reduced 13% from a 4-year high to 481k contracts as high volatility dampened leveraged fund appetite.

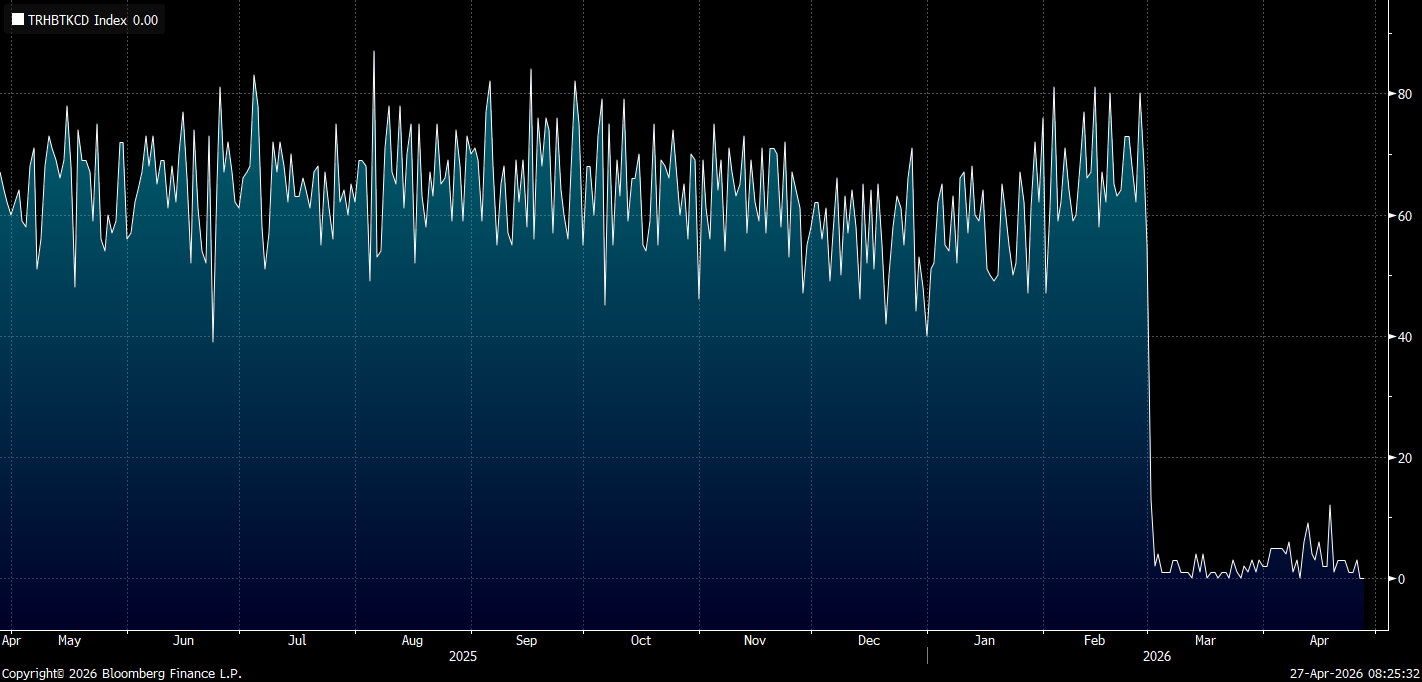

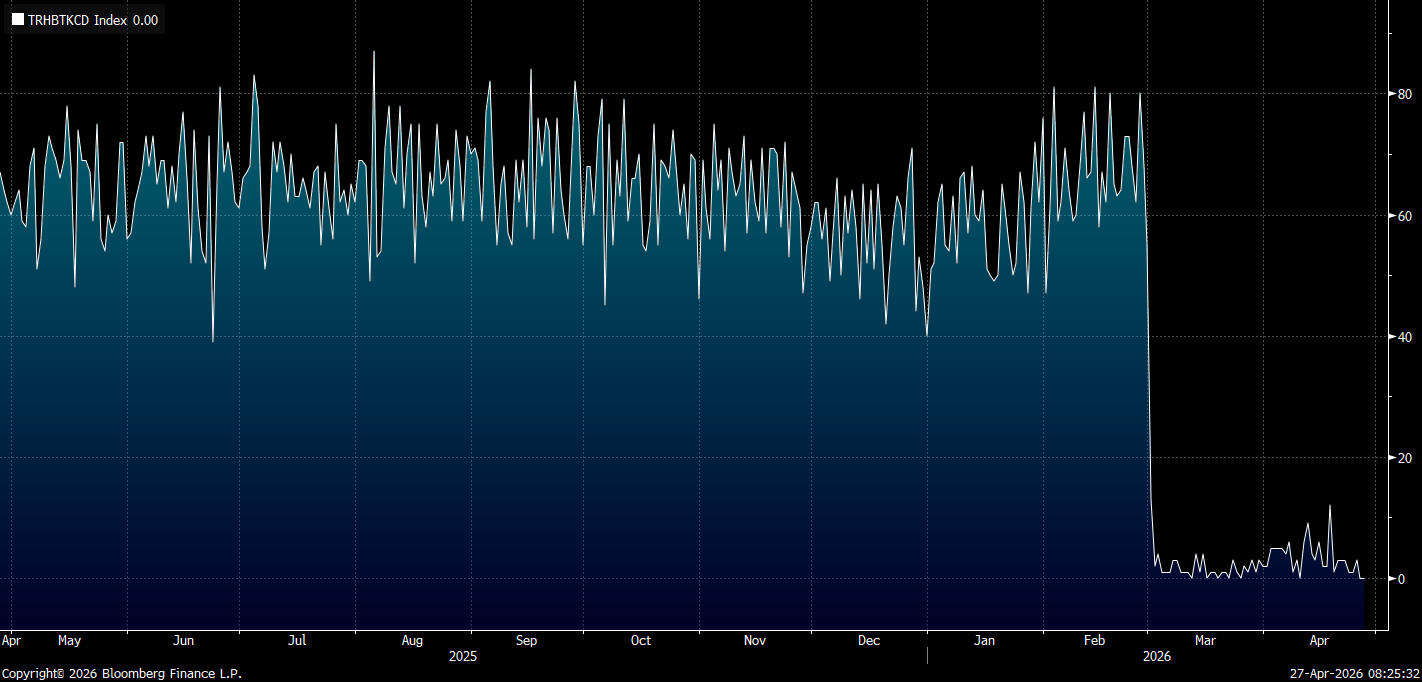

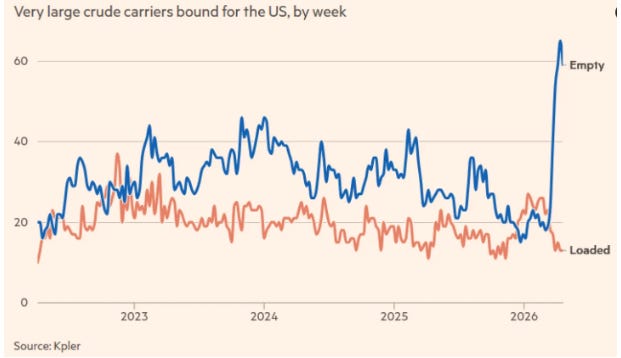

Number of tankers transiting the Strait of Hormuz. Many are heading to the US to load, which leads to second-order ramifications; if US exports rise meaningfully, there will be domestic price (increased demand) and supply ( as usage outpaces production and storage gets depleted) implications, which only have two possible end-states: higher prices/shortages domestically, or export controls. Both would be sub-optimal.

Current pricing:

Worth the read‘The Four Horsemen of the PolyCrisis: Sulphur, Naphtha, El Niño & Central Bank Amplification’

🇦🇺Craig Tindale@ctindalehttps://t.co/3SqRZ881kd5:33 AM · Apr 25, 2026 · 45K Views13 Replies · 134 Reposts · 414 Likes

🇦🇺Craig Tindale@ctindalehttps://t.co/3SqRZ881kd5:33 AM · Apr 25, 2026 · 45K Views13 Replies · 134 Reposts · 414 Likes‘THE FIVE CLOCKS AND THE SYMMETRY BREAK’

Shanaka Anslem Perera ⚡@shanaka86On March 12, Alcatel Submarine Networks declared force majeure for Persian Gulf operations and stranded its cable-laying vessel Ile de Batz off Dammam. On April 22, the IRGC-linked Tasnim News Agency published a detailed map of the seven undersea internet cables transiting the

Shanaka Anslem Perera ⚡@shanaka86On March 12, Alcatel Submarine Networks declared force majeure for Persian Gulf operations and stranded its cable-laying vessel Ile de Batz off Dammam. On April 22, the IRGC-linked Tasnim News Agency published a detailed map of the seven undersea internet cables transiting the 2:24 AM · Apr 25, 2026 · 29.9K Views9 Replies · 105 Reposts · 246 Likes

2:24 AM · Apr 25, 2026 · 29.9K Views9 Replies · 105 Reposts · 246 Likes

Ayesha Tariq, CFA@AyeshaTariqJPM's oil reports have been so informative. Yesterday's one shows global oil inventory draws accelerating from roughly balanced in January-February to 4.0 mbd in March and an extraordinary 7.1 mbd in April, with crude on water and non-OECD commercial stocks bearing the heaviest

Ayesha Tariq, CFA@AyeshaTariqJPM's oil reports have been so informative. Yesterday's one shows global oil inventory draws accelerating from roughly balanced in January-February to 4.0 mbd in March and an extraordinary 7.1 mbd in April, with crude on water and non-OECD commercial stocks bearing the heaviest 2:59 PM · Apr 24, 2026 · 24.6K Views6 Replies · 59 Reposts · 226 Likes

2:59 PM · Apr 24, 2026 · 24.6K Views6 Replies · 59 Reposts · 226 Likes Policy Tensor@policytensorI spoke with a macro hedge fund manager who manages billions in assets this week. He had reached out to talk about the war. One pushback he had has stayed with me. He said he agreed that the US has been defeated; that the mature-strike regime necessarily meant that the world is

Policy Tensor@policytensorI spoke with a macro hedge fund manager who manages billions in assets this week. He had reached out to talk about the war. One pushback he had has stayed with me. He said he agreed that the US has been defeated; that the mature-strike regime necessarily meant that the world is Policy Tensor @policytensorI’ve seen this argument over and over. “You’re assuming that they are rational.” What is required for analytical purposes is a very weak form of rationality: the politician or the military man wants to win, wants an advantage; not that he is not going to make serious errors.6:27 AM · Apr 25, 2026 · 167K Views79 Replies · 180 Reposts · 798 Likes

Policy Tensor @policytensorI’ve seen this argument over and over. “You’re assuming that they are rational.” What is required for analytical purposes is a very weak form of rationality: the politician or the military man wants to win, wants an advantage; not that he is not going to make serious errors.6:27 AM · Apr 25, 2026 · 167K Views79 Replies · 180 Reposts · 798 Likes Gordon Johnson@GordonJohnson191/7 Market Outlook — Structural Dislocation in U.S. Equities Here's how @GLJ_Research is reading the setup heading into next week. Our core thesis is that the U.S. equity market is currently exhibiting what we'd characterize as a structural dislocation between price discovery6:52 PM · Apr 24, 2026 · 20.9K Views17 Replies · 23 Reposts · 130 Likes

Gordon Johnson@GordonJohnson191/7 Market Outlook — Structural Dislocation in U.S. Equities Here's how @GLJ_Research is reading the setup heading into next week. Our core thesis is that the U.S. equity market is currently exhibiting what we'd characterize as a structural dislocation between price discovery6:52 PM · Apr 24, 2026 · 20.9K Views17 Replies · 23 Reposts · 130 Likes

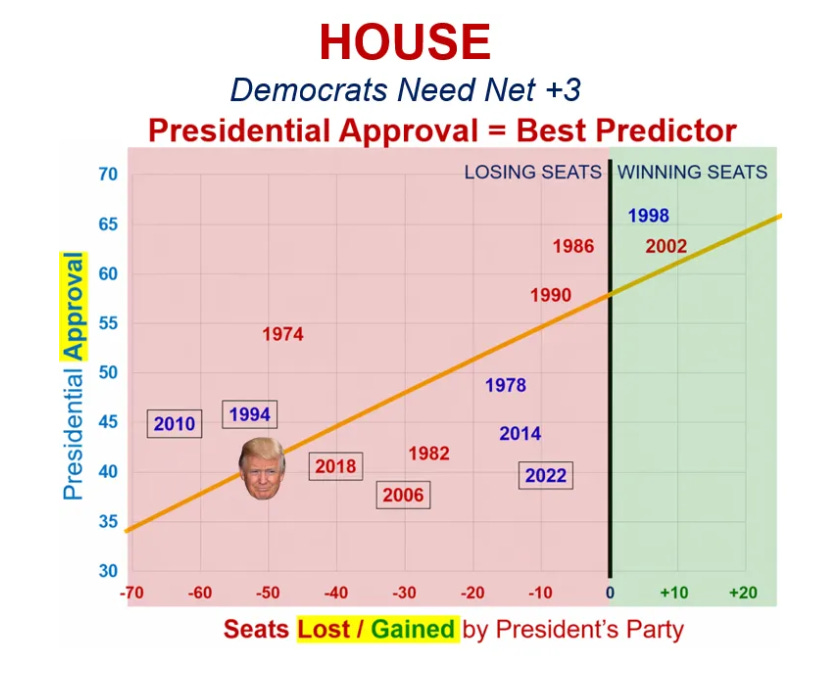

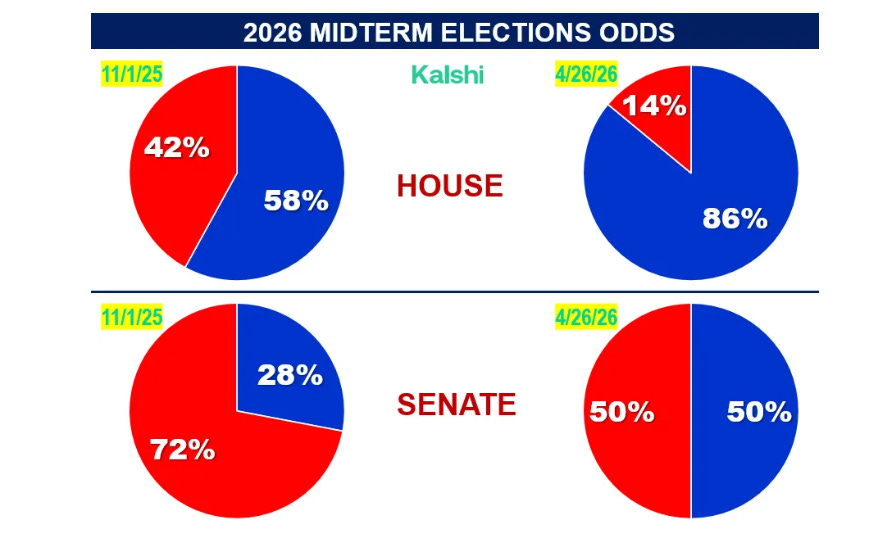

Always keep one eye on this.