خیلی برنده شدن

morning musings 4.9.26

SO MUCH WINNING

KEY THEMES

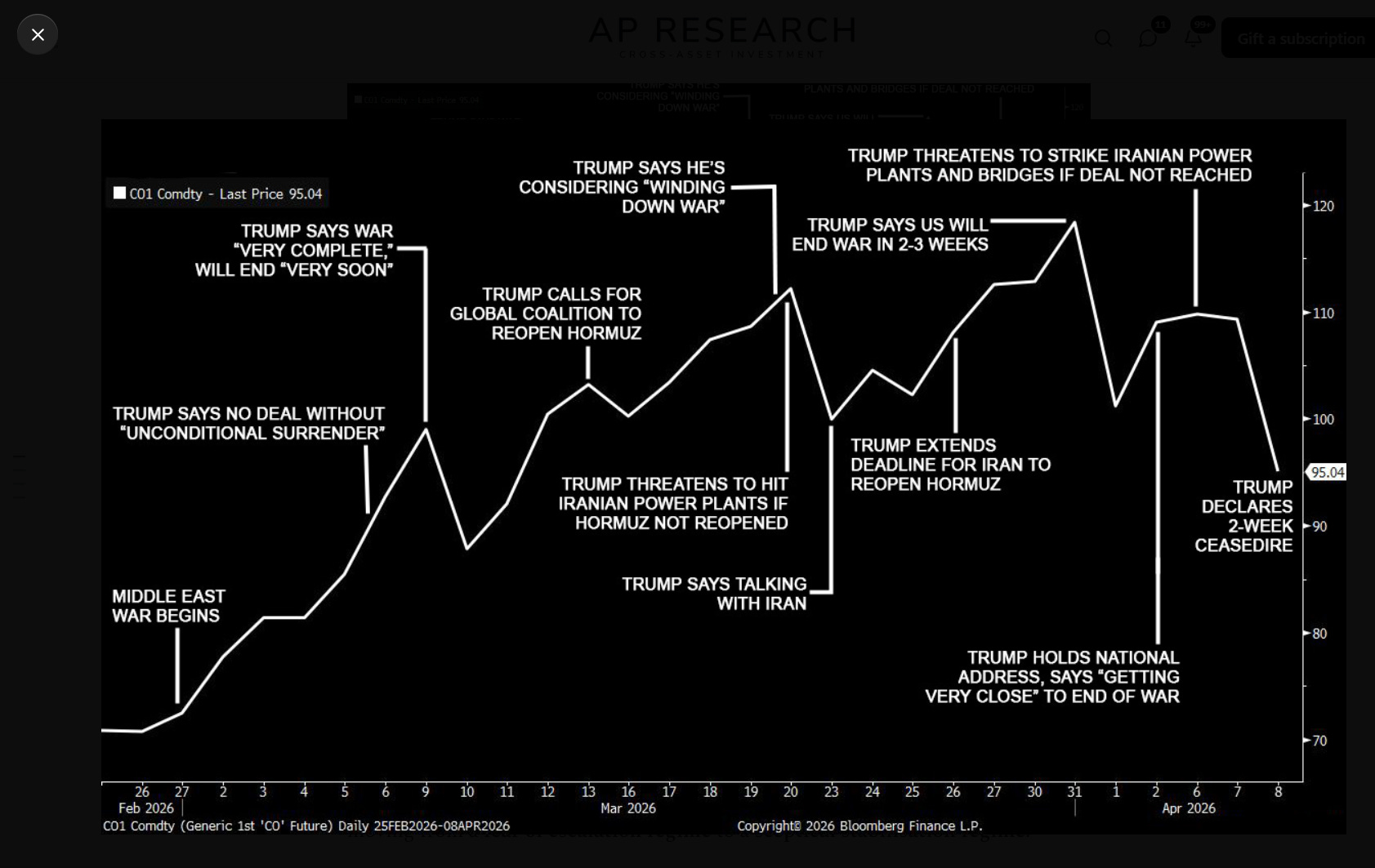

Markets have already priced in the best-case Iran scenario, leaving equities vulnerable to any deterioration in talks . Price action overnight was striking—positive ceasefire sentiment continues to dominate despite consistently negative news flow, raising questions about how much optimism is already priced in.

US-Iran ceasefire is already showing cracks; markets reverse Wednesday’s relief rally, with oil rebounding toward $98/barrel and stocks retreating as Tehran warns parts of the deal have been breached.

Iran limiting Hormuz passage to around a dozen ships daily and charging tolls.

Brent crude jumped back after its biggest one-day drop since April 2020, as the Strait of Hormuz remains largely blocked and Israeli strikes on Lebanon threaten to derail the truce.

President Trump reiterated keeping US military assets around Iran until a “real agreement” is reached, stating the military will stay until Iran complies

Cross-asset correlations are breaking down again; DXY higher, EMG slide 1%, and Euro banks that rallied hard on Wednesday give back ground .

MACRO

Dollar could see renewed gains if the ceasefire fails to hold or upcoming data show a sharp rise in US inflation

Fed minutes revealing policymakers expect the war-driven energy price shock to push inflation higher. Many policymakers cited the possible need for interest rate hikes to counter the risk of sustained inflation from high oil price

New York Fed’s Survey of Consumer Expectations

US consumers expected an inflation rate of 3.4% over the next 12 months, up 0.4 percentage points from February—the largest monthly increase in a year—according to the

Three-year inflation expectations accelerated to 3.1% from 3.0%, while five-year expectations remained at 3.0%

Physical-Paper Oil Market Disconnect: Dated Brent (physical crude) hit a record $144.42/barrel (now down to $124)while futures traded near $110, highlighting extreme supply tightness in real-world barrels versus paper market optimism . This disconnect suggests significant upside risk if the ceasefire fails.

GS lowered its oil price forecasts for Q2 2026, expecting Brent crude to average $90 per barrel, down from a previous estimate of $99.

Asian refiners are contemplating 20-30% run rate cuts and accelerated maintenance schedules as dozens of crude tankers remain stranded in the Persian Gulf

Alternative Atlantic Basin barrels carry prohibitively high freight premiums, creating a severe margin squeeze for refiners

Iran war doubled Russia’s main oil revenue to USD 9bn in April, Reuters reports based on its calculations.

‘Iran Tightens Its Grip on Hormuz Despite Cease-Fire’ (wsj)

‘The Fragile Peace’ (Campbell)

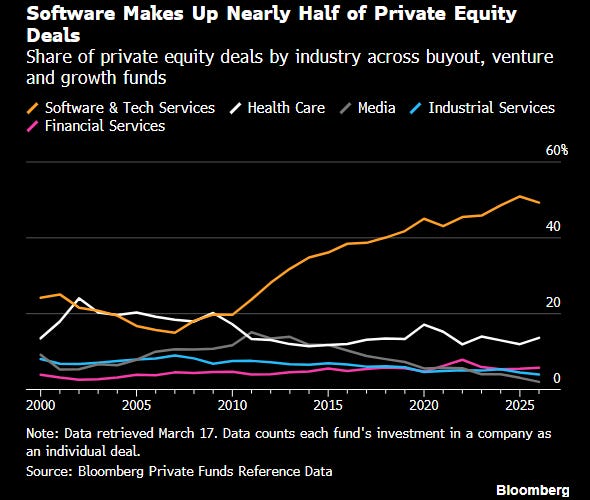

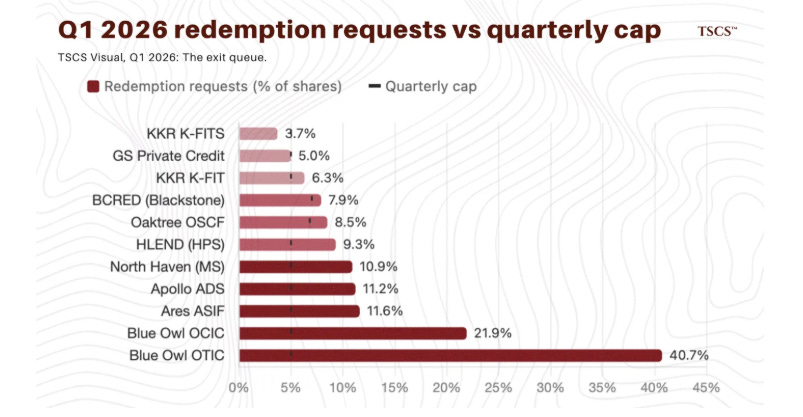

Private Credit issues continue apace

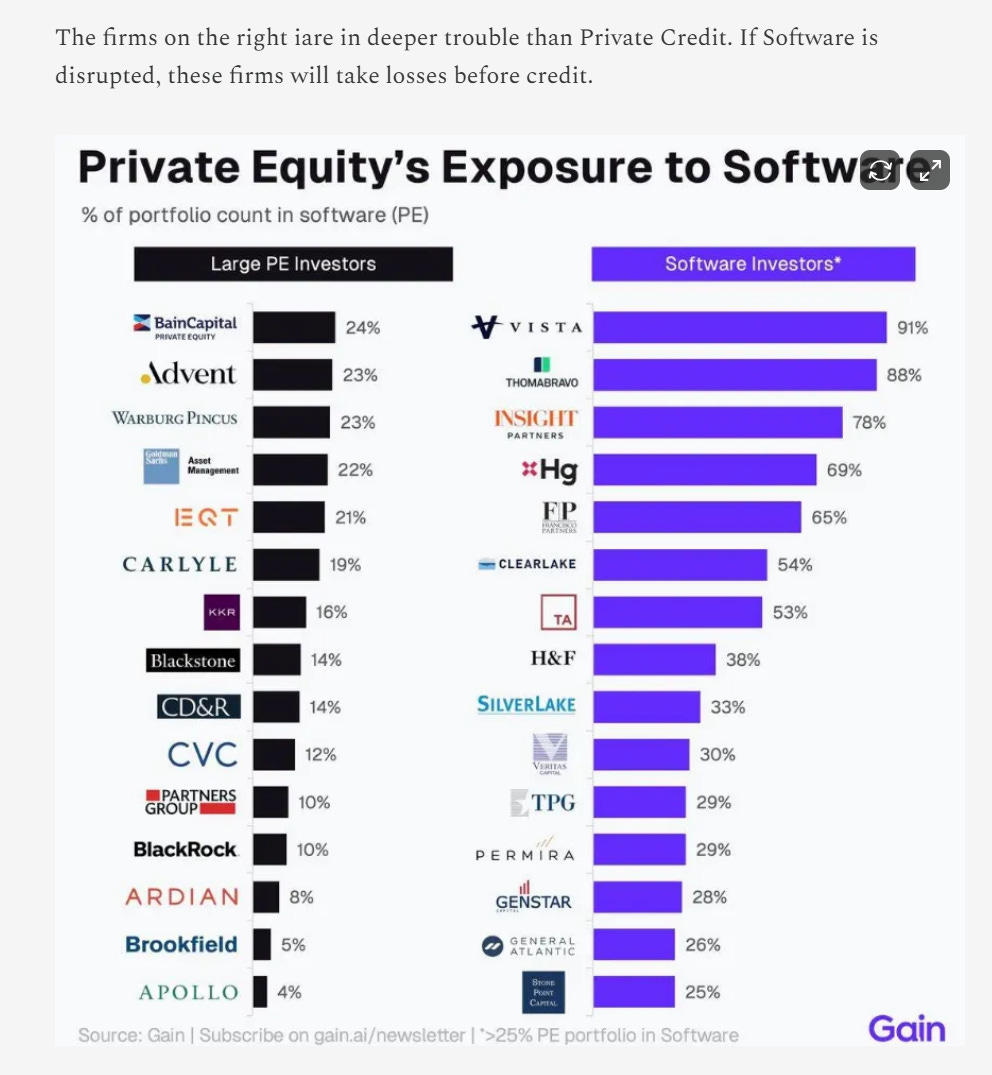

‘Private Markets’ Software Pain Is About to Get a Lot Worse’: ‘A wall of debt maturities is looming for the private markets industry, with more than $330 billion of high yield, leveraged loan and business development company-linked software and technology debt coming due for repayment through 2028.’ (bbrg)

‘MFS: British Cousin to First Brands & Tricolor’ (Debt Serious)

‘Private Markets’ Software Pain Is About to Get a Lot Worse’

‘Trapped in Private Credit’ (TSCS)

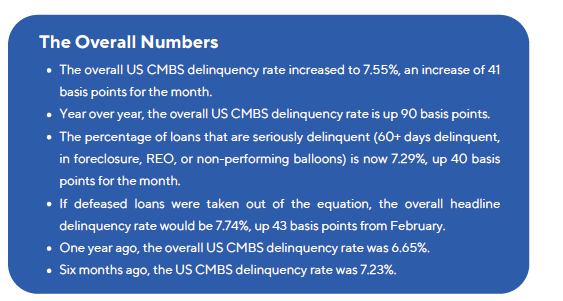

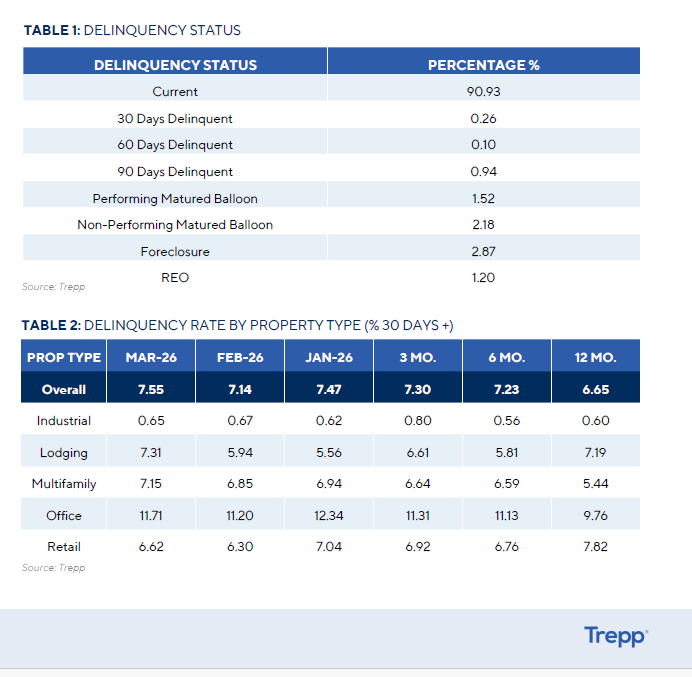

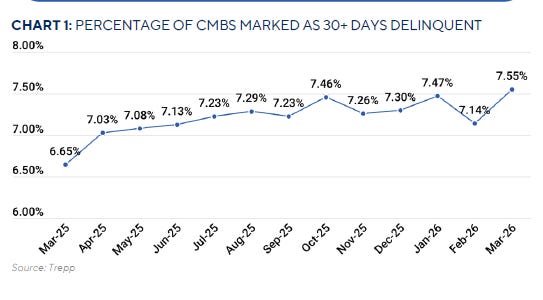

And let’s not forget about CRE!! From Trepp:

SPX remains in 6 month ‘box; is it distribution top or measured move ‘flag’ pattern?

Financials kick off earnings on Monday- will this rally off support (with RSI now >60) flip the risk/reward balancwe towards ‘sell the news’?

XLF

KRE

Mega Bank outlook as we approach earnings-palooza

• JPM Q1 (Apr 14): EPS est. $5.32-5.50; NII guidance $104.5B FY2026 (plateauing); CIB fees expected mid-to-high teens YoY; ROTCE target 17-18%; Dimon “cautiously optimistic”; 17M+ customers; watch card NCOs at ~3.4% (normalization) and deposit stickiness.

• GS Q1 (Apr 13): EPS est. $15.62-15.94; divested consumer credit; ECM desk benefits from high-profile IPO pipeline; M&A; advisory described as record backlog; consensus “M&A; supercycle” in H2 2026 contingent on Fed and geo clarity.

• BAC (Apr 15): CET1 ~11.4%; Merrill Lynch AUM record $4.1T; EPS est. ~$1.00-1.01; efficiency ratio target 60%; asset sensitivity vs. Yield curve evolution remains debate; discretionary card spend +2.6% YTD (Chase data).

• Citi: ROTCE 10-11% (Fraser restructure); shares ~doubled past year; efficiency ratio as key Q1 metric.

• Regulatory: Fed re-proposed Basel III Endgame Mar 19, 2026 -- effectively lowered capital requirements for large banks.

Whitney Baker interview (on Meb Faber podcast) 100% the worth the time: ‘This Is How a Financial Empire Ends’

How Trump Took the U.S. to War With Iran (NYT)

‘The Big Thing: We Are In A World War That Isn’t Going To End Anytime Soon.’ (Dalio)

‘Trump Derangement Syndrome’ (Notes from the Circus)

‘Perspective: Uncertainty suits neither quantitative modeling nor hyperbole’

‘The end of the war, not the regime’ (Andrew Fox)

‘My overall assessment is blunt. Militarily, this was a limited US-Israeli success. Huge tactical wins across the board: Iran’s military and industrial infrastructure has sustained significant damage, and Israel is more secure in the short term. Politically, Iran achieved the one outcome its leaders value most: regime survival. Strategically, the situation remains unstable because the nuclear issue is unresolved, the future of Hormuz is uncertain, Lebanon continues to erupt, and the IRGC appears stronger than before in terms of domestic influence. Economically, the war was disastrous and widely disliked globally, with economic and diplomatic costs that will endure long after the ceasefire ends. The conflict might be coming to an end, but a prolonged solution is not yet in sight.’

")

")

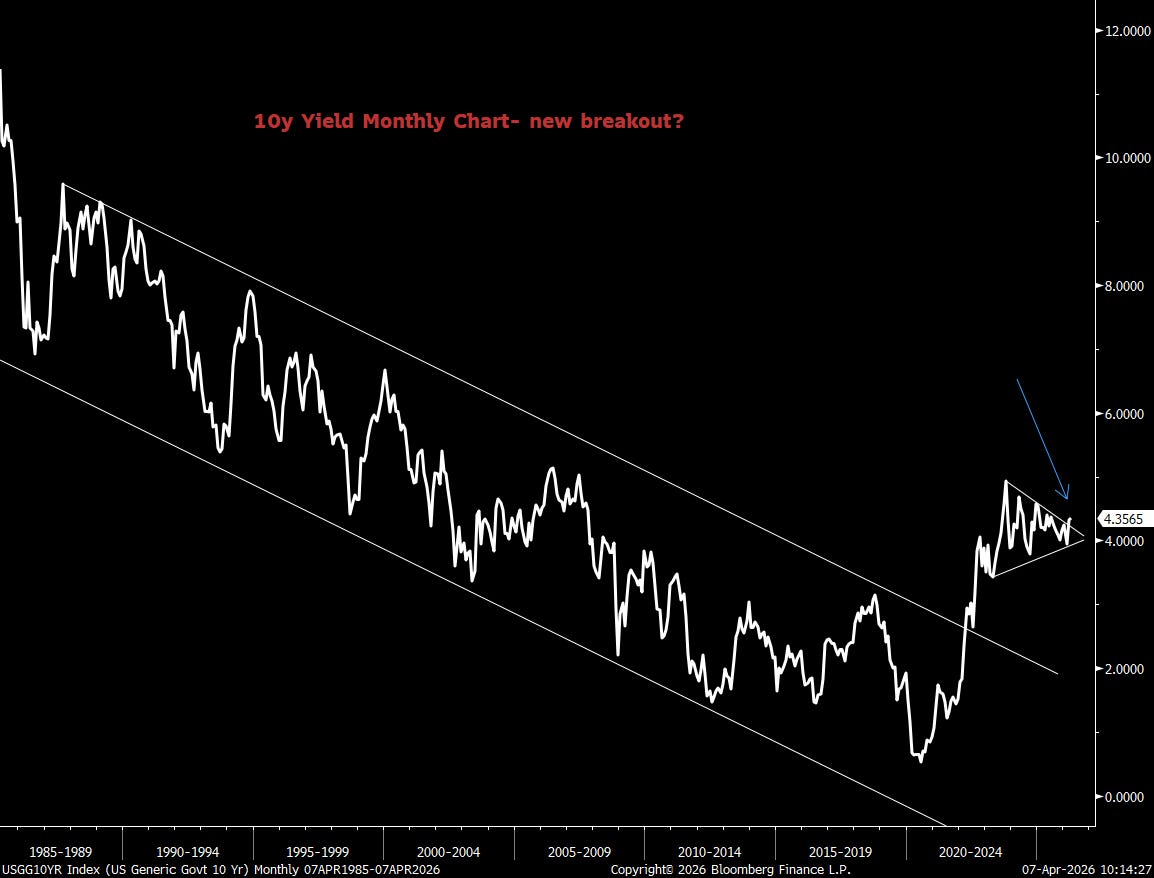

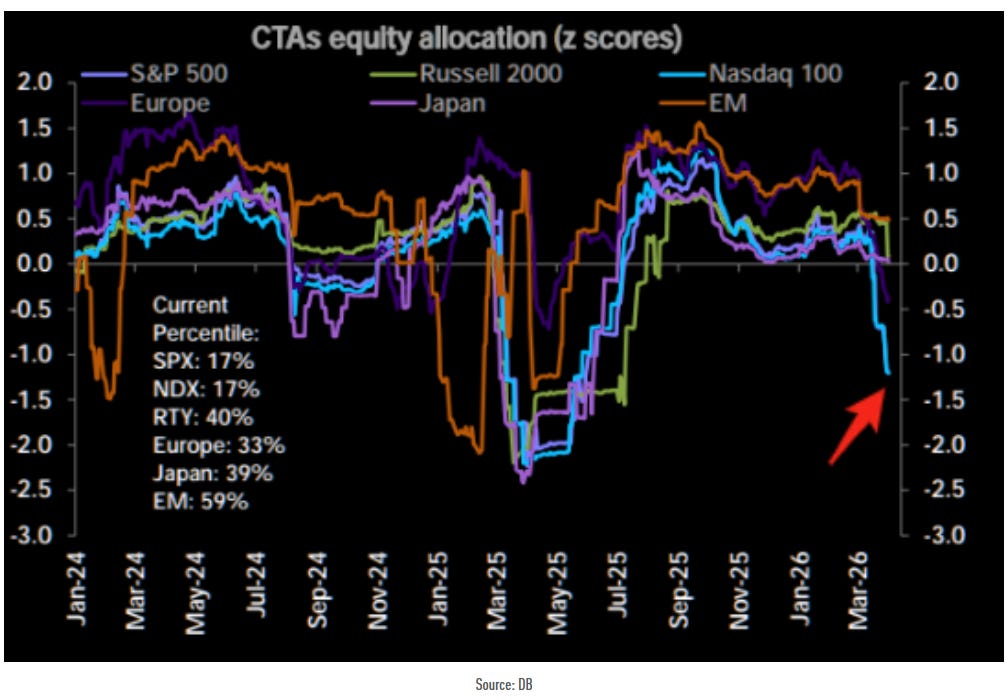

From Andrew Sarna’s Off the Charts

")